Take Control of your Future

With a low cost of entry, minimal overhead, and unlimited earning potential the Murphy Business Broker Franchise can be a very lucrative business opportunity.

Murphy Business Brokers often start as home-based businesses, this allows you to keep your overhead low, while you focus on growth and maximize your profits. You don’t need employees, there’s no inventory to maintain or equipment to purchase.

Our flexible franchise business model allows you to choose how you want to structure your business and how quickly you want to grow it. Do you want to be a sole proprietor? Maybe add an agent or two as you build out your market? Or do you see yourself building a team of agents in multiple territories? The choice is yours. And if you add agents, we’ll train them for you.

With a low cost of entry, minimal overhead, and unlimited earning potential the Murphy Business Broker Franchise can be a very lucrative business opportunity.

Murphy Business Brokers often start as home-based businesses, this allows you to keep your overhead low, while you focus on growth and maximize your profits. You don’t need employees, there’s no inventory to maintain or equipment to purchase.

Our flexible franchise business model allows you to choose how you want to structure your business and how quickly you want to grow it. Do you want to be a sole proprietor? Maybe add an agent or two as you build out your market? Or do you see yourself building a team of agents in multiple territories? The choice is yours. And if you add agents, we’ll train them for you.

While we are one of the most affordable business franchise opportunities, new franchisees still need adequate capital to invest in a franchise and establish their business.

To purchase a Murphy Business Broker Franchise you’ll need access to at least $50,000 in liquid capital and a minimum net worth of $250,000.

How much can you make?

The only earnings claims that franchisors can legally share with prospects must be included in their Item 19. If a franchisor does not include Item 19 in their Franchise Disclosure Document (FDD) you may want to explore why they exclude it.

When considering different business franchise opportunities be aware that franchisors have options for how they present this information making it sometimes difficult to compare one brand to another. For example, some do not include underperforming units or inflate their averages by including corporate-owned units that may be significantly larger and have decades of experience. Some report Average Gross Profits (AGP) while others report Average Unit Revenue (AUR).

We want you to have the information you need to make an informed decision, here’s our Item 19 in its entirety, if you have any questions just give us a call.

Item 19

Financial Performance Representation

The FTC’s Franchise Rule permits a franchisor to provide information about the actual or potential financial performance of its franchised and/or franchisor-owned outlets, if there is a reasonable basis for the information, and if the information is included in the disclosure document. Financial performance information that differs from that included in Item 19 may be given only if: (1) a franchisor provides the actual records of an existing outlet you are considering buying; or (2) a franchisor supplements the information provided in this Item 19, for example, by providing information about possible performance at a particular location or under particular circumstances.

The data used in preparing this financial performance representation was compiled from information submitted to us by the franchisees in the closing submissions reports. The figures in the tables below have not been audited. Written substantiation of the data used in preparing this financial performance representation will be made available to a prospective franchisee on reasonable request.

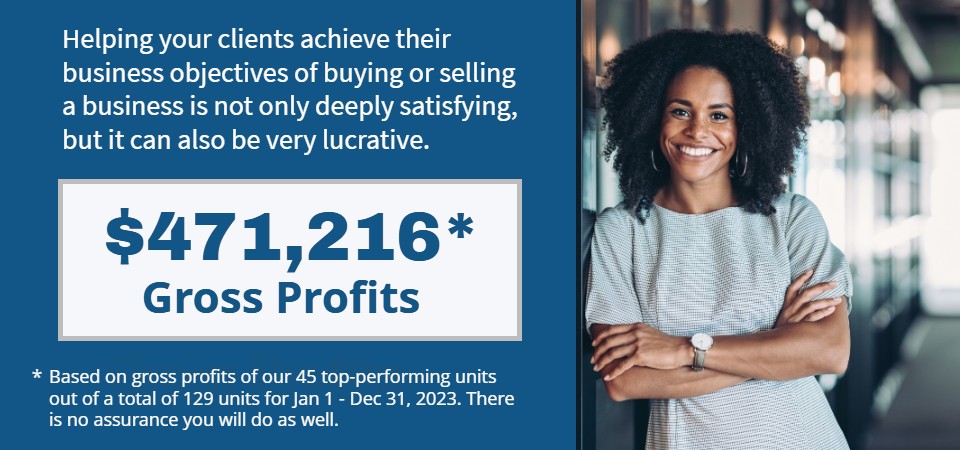

There were 134 Murphy Business franchise units in operation as of January 1, 2023. Of those, 5 were terminated or expired and were not renewed during 2023. On December 31, 2023, our fiscal year end, there were 133 franchise units in operation. The following financial performance representation includes the 129 franchise units that began operation on or before January 1, 2023 and operated continuously through December 31, 2023. 9 franchise units were excluded because they were not in operation for a full year, 4 of which were new to the System, 1 of which temporarily suspended operations due to a state licensing issue. Some of our franchisees operate multiple franchise units, each pursuant to a separate franchise agreement. Each multi-unit franchisee, however, provides us with a combined financial report that consolidates the gross revenue of all of their franchise units. The typical time for a Murphy Business franchise to close on their first business transfer is 7-9 months, however, they are able to generate revenue from other ancillary services. Below is 2023 Gross Profit data for our 129 franchise units that operated the full 12 months from January 1 – December 31, 2023. Gross Profit means all revenue and receipts derived from the franchisee’s operation of the Murphy Business, less the 10% royalty paid to us.

Top, Middle, and Low Thirds

* 5 franchisees each operate 2 franchise units and 1 franchisee operates 4 units

** 7 franchisees operates 2 franchise units

*** 1 franchisee operates 3 franchise units and 1 franchisee operates 2 units

Sole Proprietor vs. Office with Agents

Some franchisees operate as sole proprietors and some operate with independent contractor agents. The table below shows Average Gross Profits as outlined above for the two different operating methods.

We strongly suggest that you consult your own financial advisor or personal accountant concerning financial projections.

Written substantiation for the financial performance representation will be made available to the prospective

franchisee upon reasonable request.

Some franchisees have achieved these Gross Profits. Your individual results may differ. There is no assurance that you’ll earn as much.

Other than the preceding financial performance representation, we do not make any financial performance representations. We also do not authorize our employees or representatives to make any such representations either orally or in writing. If you are purchasing an existing franchise, however, we may provide you with the actual records of that franchise. If you receive any other financial performance information or projections of your future income, you should report it to our management by contacting Thomas J. Coba, CEO, Murphy Business & Financial Corporation LLC, 407 N. Belcher Road, Clearwater, FL 33765, 727-725-7090, the Federal Trade Commission, and the appropriate state regulatory agencies.

How Much Does It Cost To Become A Murphy Business Broker?

With an Initial Franchise Fee starting at 40K* and Low Overhead Costs you can be in business as a Murphy Business Broker for under 100K.

*Please see Items 5, 6, and 7 in our FDD for more details